Income Tax

Old vs New Income Tax Act 2025: Tax Payments, Collection & Refunds Explained (2026 Transition Guide)

CK

Compliance Katta3 min read

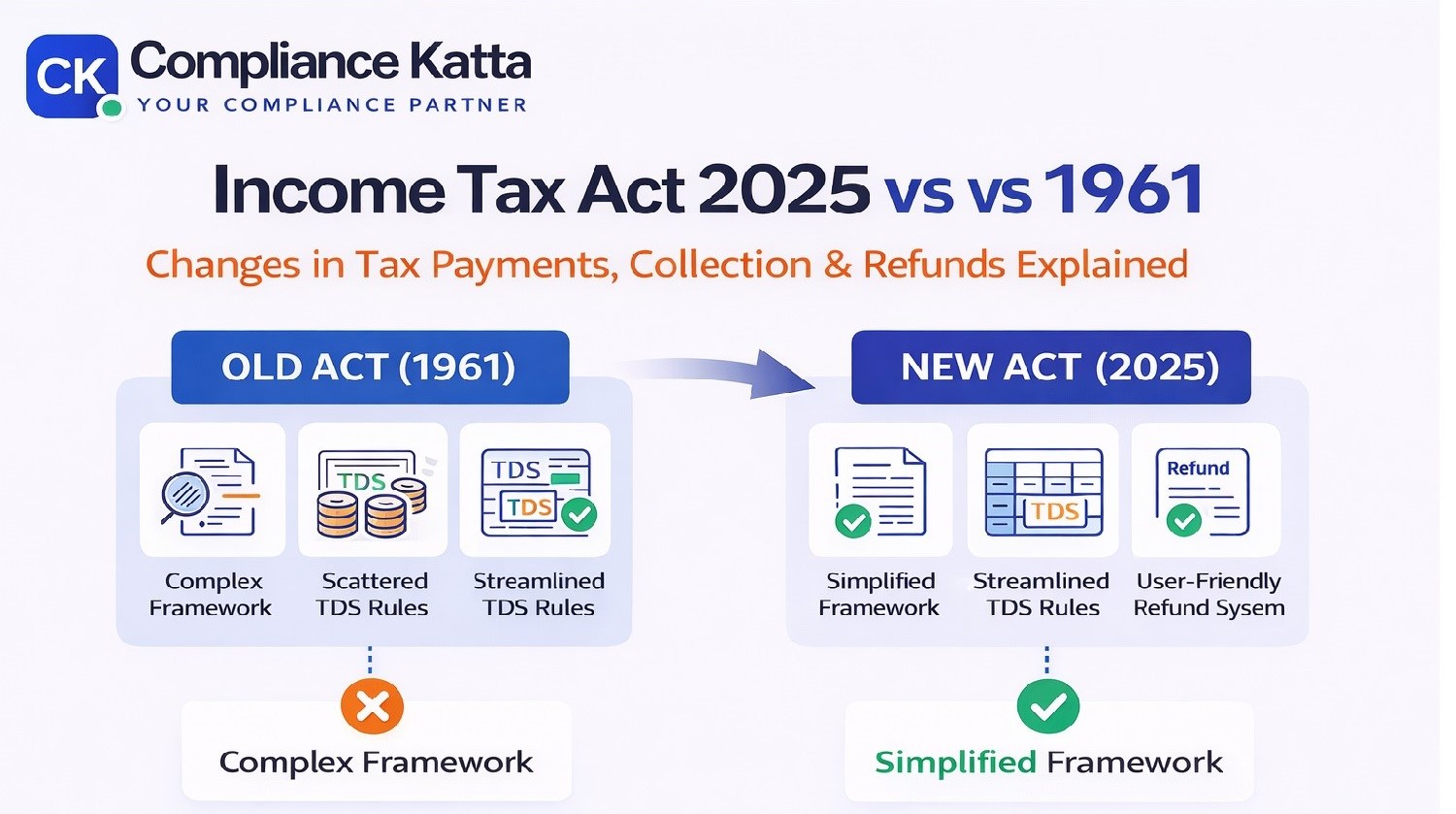

The Income Tax Act, 2025 (effective from 1 April 2026) replaces the 1961 Act with a simplified and structured approach. While the core tax system remains unchanged, the new law focuses on clarity, simplification, and digital alignment.

Old Act (1961) → Complex Sections → Multiple References → Confusion ⬇ New Act (2025) → Simplified Structure → Tabular Format → Easy Compliance

| Particulars | Old Act (1961) | New Act (2025) |

|---|---|---|

| Basic Framework | TDS, Advance Tax, Self-Assessment | Same structure continues |

| Payment Modes | Bank / Online | No change |

| Advance Tax | Based on Assessment Year | Shift to Tax Year concept |

| Due Dates | 15 Jun, Sep, Dec, Mar | Same dates continue |

| Computation | Complex provisions | Formula-based (Section 405) |

👉 Key Insight: No major policy change, but structure is simplified and easier to understand. :contentReference[oaicite:0]{index=0}

| Particulars | Old Act | New Act |

|---|---|---|

| TDS Sections | Multiple sections (192–194T) | Consolidated into Sections 392 & 393 |

| Rates & Thresholds | Defined separately | Largely unchanged |

| Structure | Scattered provisions | Tabular format (Resident / Non-resident) |

| Interest on Delay | 1% / 1.5% per month | No change |

| Transition Rule | NA | Depends on date of payment/credit |

👉 Key Insight: System remains same but presentation is simplified and consolidated. :contentReference[oaicite:1]{index=1}

👉 This ensures smooth transition without compliance confusion. :contentReference[oaicite:2]{index=2}

| Particulars | Old Act | New Act |

|---|---|---|

| Pending Refunds | Processed under old Act | Still valid under new Act |

| Excess TDS Refund | Claim within time limit | Still allowed (Form 26B) |

| Time Limit | 2 years | No change |

👉 Key Insight: No taxpayer loses refund rights due to new law. :contentReference[oaicite:3]{index=3}

👉 Ensures continuity in tax administration. :contentReference[oaicite:4]{index=4}

✔ No major change in tax payment system ✔ TDS simplified & consolidated ✔ Refund rights fully protected ✔ Transition rules clearly defined ✔ Focus on simplicity & digital compliance

Need help with Income Tax compliance? 📞 +91 76662 49690 📧 contact@compliancekatta.com

No, the core system (TDS, TCS, advance tax, self-assessment) remains unchanged.

TDS sections are consolidated into fewer sections and presented in tabular format for simplicity.

Yes, any pending tax liability under the old Act remains payable and recoverable.

Yes, refund claims under the old Act remain valid even after 1 April 2026.

The applicable law depends on the date of income/payment—not the filing date.