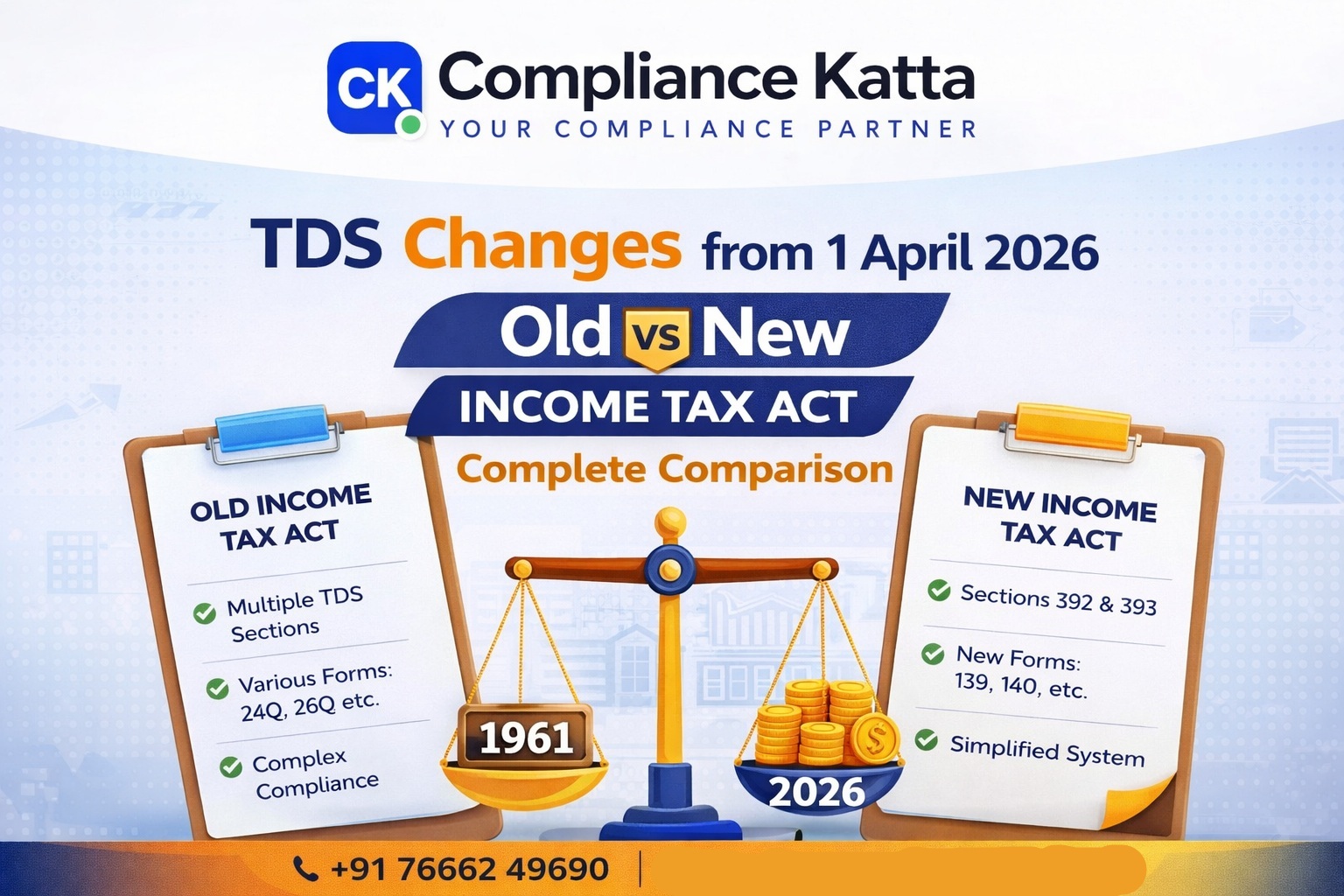

TDS Changes from 1 April 2026 – Old vs New Income Tax Act

The Income Tax Act, 2025 has replaced the Income Tax Act, 1961 effective from 1st April 2026. While the structure of TDS provisions has changed significantly, the core tax rates and thresholds largely remain the same.

📊 Key Highlight

- No major change in TDS rates or thresholds

- Simplification of provisions through tabular format

- New section structure introduced

- New forms and compliance system implemented

🔍 Comparative Analysis: Old vs New TDS Provisions

| Particulars | Old Act (1961) | New Act (2025) |

|---|---|---|

| TDS Sections | Multiple sections (192 to 194T) | Consolidated into Section 392 & 393 |

| Structure | Complex and scattered | Simplified and tabular format |

| TDS Rates | Defined under various sections | No change in rates |

| Threshold Limits | Different for each section | Same as old Act |

| Applicability | Based on payment/credit | Same concept retained |

| Forms | 24Q, 26Q, 27Q etc. | Form 138, 140, 144 etc. |

| Challan-cum Statement | Multiple forms (26QB, 26QC, etc.) | Single Form 141 |

| Compliance System | Complex reporting | Simplified & digital-friendly |

📌 Major Changes Explained

1. Consolidation of TDS Sections

All TDS provisions from Sections 192 to 194T are now merged into:

- Section 392 – Salary

- Section 393 – Other payments

This improves clarity and reduces confusion. :contentReference[oaicite:0]{index=0}

2. No Change in TDS Rates

The government has clearly stated that TDS rates and thresholds remain unchanged. The reform focuses only on simplification. :contentReference[oaicite:1]{index=1}

3. Transition Rule (Most Important)

TDS applicability depends on:

- If payment/credit is before 31 March 2026 → Old Act applies

- If payment/credit is after 1 April 2026 → New Act applies

This is based on the "earlier of payment or credit" rule. :contentReference[oaicite:2]{index=2}

4. New TDS Return Forms

- Old Forms: 24Q, 26Q, 27Q

- New Forms: 138, 140, 144

This applies from Q1 of Tax Year 2026-27. :contentReference[oaicite:3]{index=3}

5. Due Dates – No Change

TDS deposit due dates remain same:

- 7th of next month

- March TDS → 30th April

Only governing Act changes after April 2026. :contentReference[oaicite:4]{index=4}

6. ERP & System Updates Required

Businesses must update systems to reflect new section numbers and forms. :contentReference[oaicite:5]{index=5}

⚠️ Important Compliance Points

- Wrong section quoting may lead to return errors

- Both Acts will run parallel during transition

- Correction returns must be filed under respective Act

- TDS credit will be mapped based on year

📢 Conclusion

The TDS changes from 1 April 2026 are structural, not financial. The aim is to simplify compliance without changing tax burden. Businesses should focus on updating systems and understanding new section mapping.

🔗 Stay Updated with Compliance Katta

For professional assistance, contact us at, Services started @ Rs. 499 Compliance Katta 📞 +91 76662 49690

Common Questions

Q.Is there any change in TDS rates from 1 April 2026?

No, TDS rates and thresholds remain unchanged under the new Income Tax Act.

Q.What is the biggest change in TDS provisions?

The biggest change is consolidation of sections into Section 392 (salary) and Section 393 (other payments).

Q.Which Act applies during transition period?

It depends on the earlier of payment or credit: Before 31 March 2026 → Old Act After 1 April 2026 → New Act

Q.Are TDS return forms changing?

Yes, new forms like Form 138, 140, and 144 replace old forms like 24Q and 26Q.

Q.Do businesses need to update their systems?

Yes, ERP and payroll systems must be updated for new sections, forms, and compliance requirements.