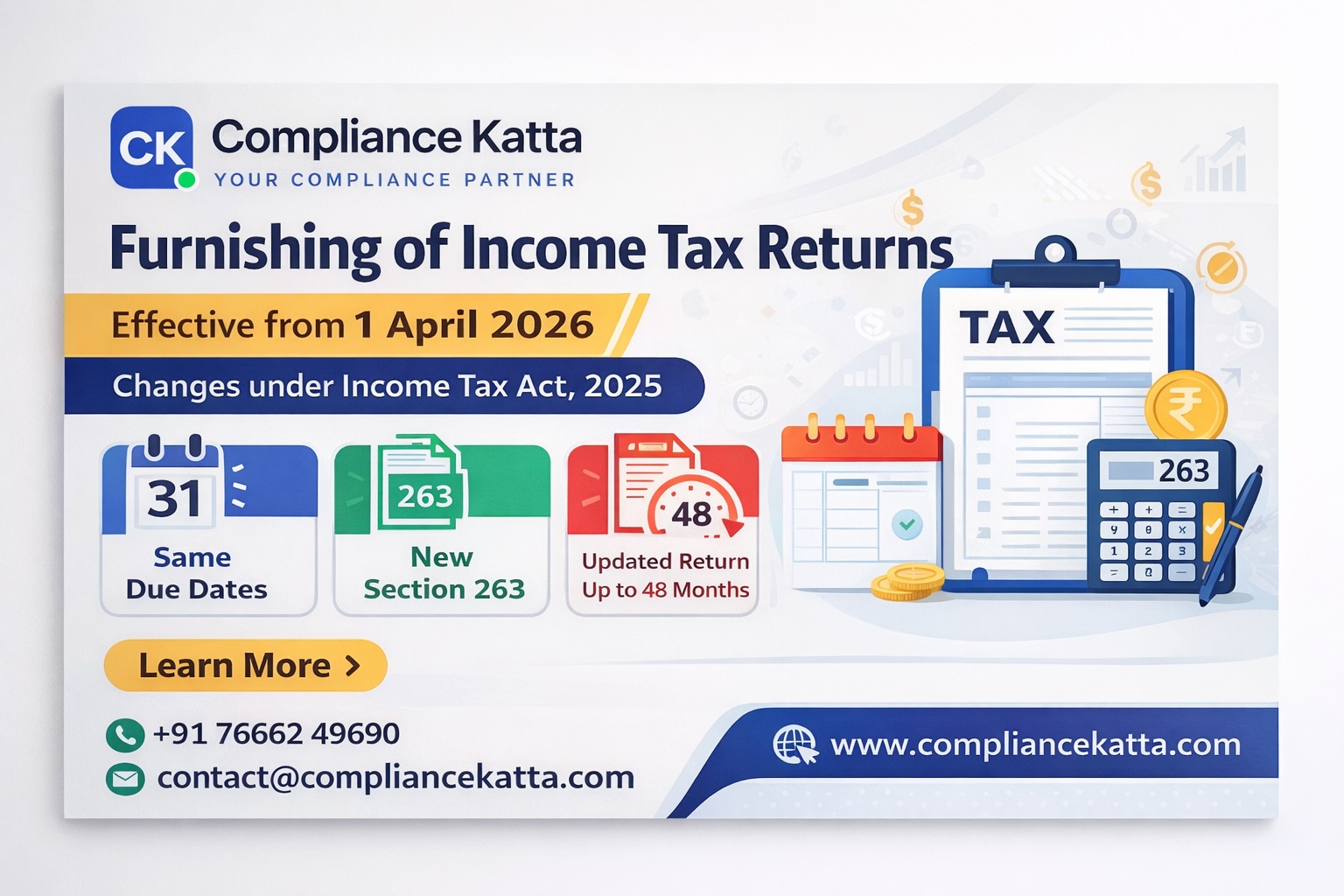

Furnishing of Income Tax Returns under Income Tax Act, 2025

The process of furnishing Income Tax Returns (ITR) continues to remain one of the most important compliance requirements for taxpayers. With the introduction of the Income Tax Act, 2025 (effective from 1 April 2026), certain structural improvements have been made while keeping the core framework largely unchanged.

🔍 Key Highlights

- All provisions related to ITR filing are now consolidated under Section 263.

- Types of returns include:

- Original Return

- Belated Return

- Revised Return

- Updated Return (ITR-U)

- Basic filing obligations remain similar to the old Income Tax Act, 1961.

📅 Due Dates for Filing ITR

| Category | Due Date |

|---|---|

| Individuals (Non-audit cases) | 31st July |

| Business (Non-audit) | 31st August |

| Audit Cases / Companies | 31st October |

| Transfer Pricing Cases | 30th November |

Note: Due dates remain same as earlier law.

📌 Types of Returns

1. Original Return

Filed within the due date as prescribed under Section 263(1).

2. Belated Return

Can be filed within 9 months from the end of the tax year or before assessment completion.

3. Revised Return

Can be filed within 12 months from the end of the tax year or before completion of assessment.

4. Updated Return (ITR-U)

Can be filed within 48 months with additional tax liability.

⚠️ Important Compliance Points

- Filing return within due date is mandatory for carry forward of losses.

- Late filing fees:

- ₹1,000 (income up to ₹5 lakh)

- ₹5,000 (other cases)

- E-verification methods remain same (Aadhaar OTP, DSC, Net Banking).

🔄 Transition Impact (FY 2025-26 vs FY 2026-27)

- Income of FY 2025-26 → Filed under old Act (AY 2026-27)

- Income of FY 2026-27 → Filed under new Act (Tax Year 2026-27)

- No need to file two returns for same income.

📊 Practical Tips for Taxpayers

- Maintain separate records for both years.

- Reconcile Form 26AS carefully.

- File returns before due dates to avoid penalties.

- Select correct year (AY or Tax Year) on portal.

🚀 Need Help with ITR Filing?

Contact Compliance Katta 📞 +91 76662 49690 📧 contact@compliancekatta.com

Common Questions

Q.What is Section 263 in Income Tax Act, 2025?

Section 263 consolidates all provisions related to filing of income tax returns including original, belated, revised, and updated returns.

Q.Has the due date for filing ITR changed?

No, the due dates remain the same as under the previous Income Tax Act.

Q.Can I file a revised return under the new Act?

Yes, revised returns can be filed within 12 months from the end of the tax year or before assessment completion.

Q.What is the time limit for updated return (ITR-U)?

An updated return can be filed within 48 months from the end of the relevant financial year.

Q.Is filing return necessary for carry forward of losses?

Yes, filing the return within due date is mandatory to carry forward losses.