Income Tax

Furnishing of Income Tax Returns under Income Tax Act, 2025 – Complete Guide (Post 01 April 2026)

CK

Compliance Katta2 min read

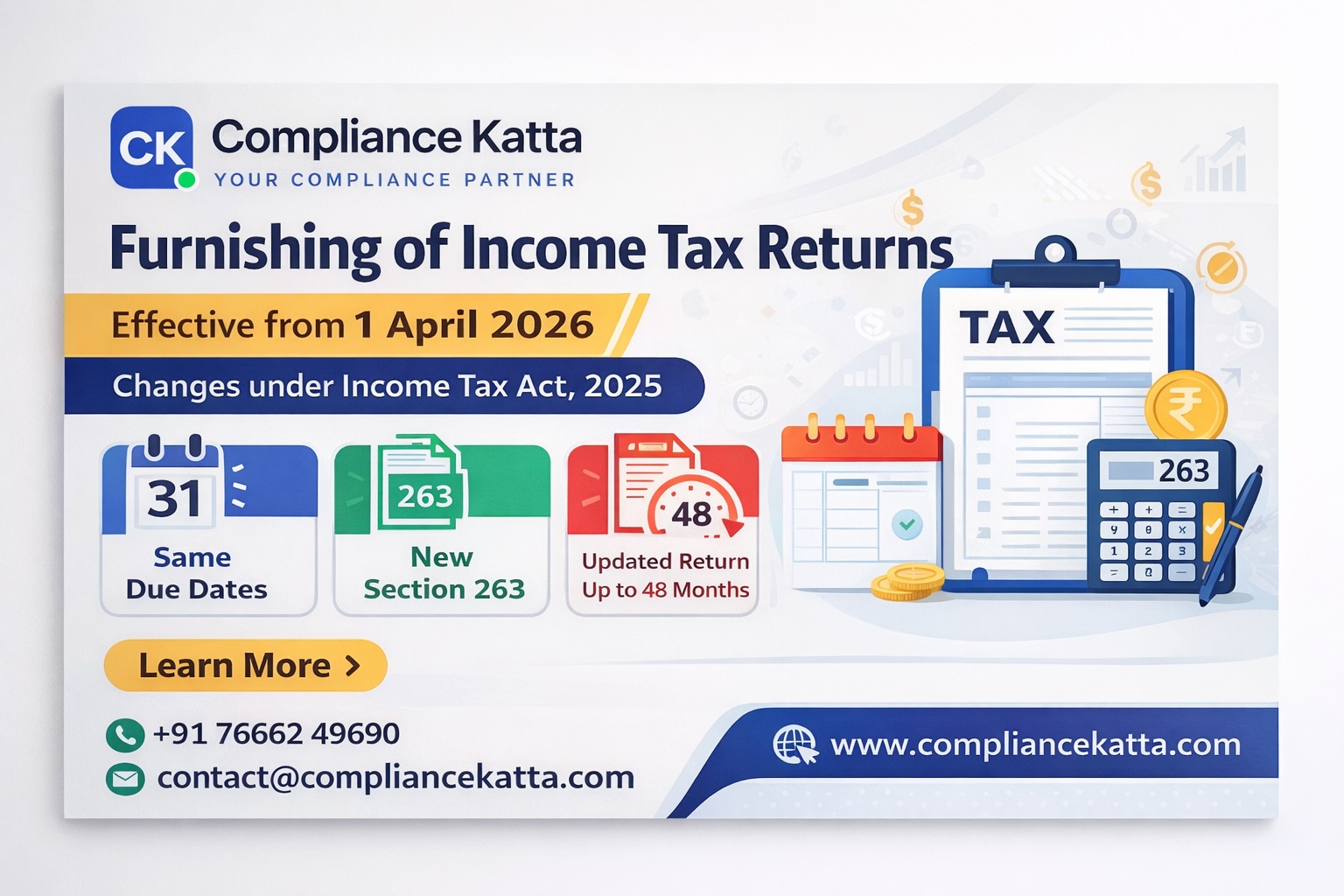

The process of furnishing Income Tax Returns (ITR) continues to remain one of the most important compliance requirements for taxpayers. With the introduction of the Income Tax Act, 2025 (effective from 1 April 2026), certain structural improvements have been made while keeping the core framework largely unchanged.

| Category | Due Date |

|---|---|

| Individuals (Non-audit cases) | 31st July |

| Business (Non-audit) | 31st August |

| Audit Cases / Companies | 31st October |

| Transfer Pricing Cases | 30th November |

Note: Due dates remain same as earlier law.

Filed within the due date as prescribed under Section 263(1).

Can be filed within 9 months from the end of the tax year or before assessment completion.

Can be filed within 12 months from the end of the tax year or before completion of assessment.

Can be filed within 48 months with additional tax liability.

Contact Compliance Katta 📞 +91 76662 49690 📧 contact@compliancekatta.com

Section 263 consolidates all provisions related to filing of income tax returns including original, belated, revised, and updated returns.

No, the due dates remain the same as under the previous Income Tax Act.

Yes, revised returns can be filed within 12 months from the end of the tax year or before assessment completion.

An updated return can be filed within 48 months from the end of the relevant financial year.

Yes, filing the return within due date is mandatory to carry forward losses.