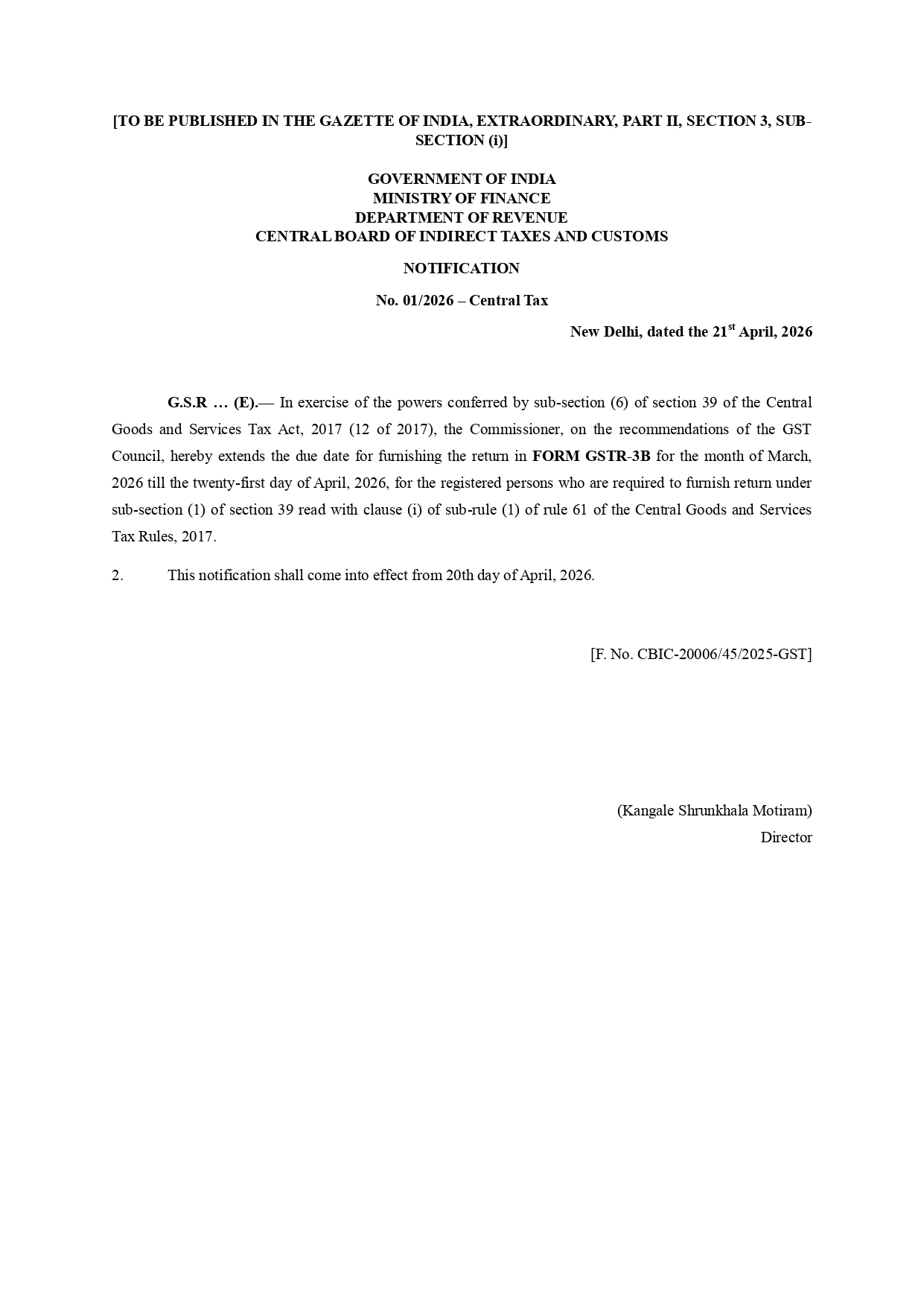

Introduction to the GSTR-3B Deadline Extension

In a significant move to ease the compliance burden on taxpayers, the Central Board of Indirect Taxes and Customs (CBIC) has announced an extension for filing the GSTR-3B return for the tax period of March 2026. According to the newly released Notification No. 01/2026-Central Tax, the deadline has been shifted to April 21, 2026. This decision was taken in rapid response to numerous reports from across India regarding severe technical glitches and complete portal crashes experienced by taxpayers on the original due date of April 20, 2026.

At Compliance Katta, we continuously monitor these regulatory shifts to ensure your business remains perfectly aligned with the latest GST mandates. This article delves deeply into the implications of this one-day extension, how it affects late fees and interest calculations, and what actionable steps your tax team should take immediately to navigate the end-of-year compliance effectively.

Key Highlights of Notification No. 01/2026-Central Tax

- Extended Due Date: The absolute deadline for filing the GSTR-3B for the crucial month of March 2026 is now officially April 21, 2026.

- Waiver of Late Fees: Taxpayers filing on or before the newly extended date will not incur the standard Rs. 50/day (or Rs. 20/day for NIL returns) late fee penalty under Section 47.

- Interest Exemption: No interest under Section 50 of the CGST Act will be levied if the tax liability is completely discharged and the return is successfully filed by April 21, 2026.

- Reason for Extension: Official acknowledgment of GSTN portal instability, providing a fair, non-penalizing opportunity for all registered businesses to fulfill their statutory duties.

Comparative Analysis: Original vs. Extended Deadline

| Compliance Parameter | Original Provision | Extended Provision (Notif 01/2026) |

|---|---|---|

| Applicable Tax Period | March 2026 | March 2026 |

| Statutory Due Date | April 20, 2026 | April 21, 2026 |

| Late Fee Applicability | Triggered from April 21, 2026 | Triggered from April 22, 2026 |

| Interest on Delayed Payment | Applicable from April 21, 2026 (@ 18% p.a.) | Applicable from April 22, 2026 (@ 18% p.a.) |

Structured Flowchart: Strategic Approach to Filing by the New Deadline

Step-by-Step Filing Workflow

- Phase 1: Reconciliation & Adjustment

- Match GSTR-1 outward supplies directly with the GSTR-3B draft.

- Reconcile auto-populated ITC in GSTR-2B with your internal purchase registers.

- Incorporate any year-end financial adjustments for FY 2025-26.

- Phase 2: Liability & Challan Generation

- Calculate net tax liability strictly after permissible ITC offset.

- Generate the PMT-06 challan on the GST portal before peak operational hours.

- Phase 3: Final Payment & Execution

- Initiate tax payment via authorized banking channels (Net Banking, NEFT/RTGS, UPI).

- Offset the recorded liability and file GSTR-3B using EVC or DSC by April 21, 2026.

Comprehensive Impact Analysis for Indian Businesses

While a 24-hour extension may initially seem nominal, its impact on corporate tax compliance, working capital management, and statutory audit preparation is profound. The end of the financial year (March 2026) represents a highly critical period requiring meticulous reconciliation of annual turnovers, ITC reversals, and comprehensive year-end adjustments. The catastrophic technical crash on April 20 threatened to impose unwarranted financial penalties and compliance ratings downgrades on millions of innocent taxpayers.

By extending the deadline to April 21, 2026, the CBIC has proactively protected businesses from the cascading effects of non-compliance. It is absolutely crucial to understand that failing to meet even this extended deadline will result in interest being calculated retrospectively from the original due date in certain interpretations, alongside mandatory late fees. Therefore, corporate finance departments must utilize this brief window not just to hastily file, but to critically ensure the accuracy of their year-end GSTR-3B. This specific return inherently forms the foundational basis for the upcoming GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement) for FY 2025-26.

Professional Tip: Do not wait until the late evening of April 21, 2026 to execute your filing. Historical data suggests the portal may experience heavy concurrent traffic once again. Generate your tax payment challans early in the business day and complete the offset process immediately to circumvent any last-minute banking integration delays.

Actionable Compliance Checklist for Taxpayers

To guarantee a flawless filing process under the newly extended timeframe, the compliance experts at Compliance Katta strongly recommend adhering strictly to the following actionable checklist:

- Verify auto-populated data: Scrutinize the liability auto-populated from your GSTR-1 to ensure it perfectly mirrors your actual outward supplies and tax invoices for March 2026.

- Reconcile Input Tax Credit (ITC): Cross-check your internal ERP books of accounts with the dynamic GSTR-2B. Claim only the strictly eligible ITC to systematically avoid future departmental scrutiny, notices, and penal interest liabilities.

- Calculate year-end adjustments: Make the necessary quantitative adjustments for credit notes, debit notes, and any inadvertently missed invoices pertaining to the closing financial year 2025-26 before finalizing the return.

- Ensure adequate cash ledger balance: If your available electronic credit ledger (ITC) does not sufficiently cover your gross liability, initiate the fund transfer to the Electronic Cash Ledger immediately to account for standard banking clearance and portal reflection times.

- Review RCM liabilities: Identify all incurred expenses that are inherently subject to the Reverse Charge Mechanism (RCM), discharge this specific liability in cash exclusively, and securely claim the corresponding ITC in the same month's return.

Warning: The official extension to April 21, 2026 applies exclusively to the GSTR-3B return for the month of March 2026. This notification does not alter, extend, or waive the statutory due dates for any other ancillary returns, TDS/TCS filings, or compliance forms under the current GST regime.

Conclusion

The CBIC's prompt issuance of Notification No. 01/2026-Central Tax provides much-needed, immediate respite to Indian businesses grappling with unpredictable GST portal inefficiencies. By strategically extending the GSTR-3B deadline to April 21, 2026, the government has demonstrated a pragmatic and taxpayer-friendly approach to systemic issues. However, businesses must remain exceptionally vigilant and execute their final filing processes efficiently within this extremely narrow window to safeguard against late fees and compounding interest.

At Compliance Katta, we are dedicated to simplifying complex statutory tax scenarios for your enterprise. Ensure your business leverages this extension wisely, and maintain robust internal reconciliation practices to definitively safeguard against future compliance hurdles and department audits.

Common Questions

Q.Who is eligible for the GSTR-3B deadline extension for March 2026?

All regular taxpayers who are mandated to file their GSTR-3B on a monthly basis are fully eligible for this extension. The CBIC provided this critical relief universally due to the GST portal's technical glitches, meaning absolutely no specific application or appeal is required to legally avail of the extended deadline of April 21, 2026.

Q.Will I be charged a late fee if I file my GSTR-3B on April 21, 2026?

No, you will not be charged any late fee if you successfully file your GSTR-3B for March 2026 on or before April 21, 2026. The official notification effectively waives the standard Section 47 late fees that would typically apply immediately after the original April 20 deadline.

Q.Does the extension to April 21, 2026, also waive the interest on delayed tax payment?

Yes, as long as your total tax liability is completely paid and the GSTR-3B return is successfully filed on or before the extended deadline of April 21, 2026, no interest under Section 50 of the CGST Act will be levied. However, any filing delay pushing past April 21 will immediately attract an 18% annual interest rate on the net cash liability.

Q.What should businesses do if the GST portal crashes again on the extended date?

Businesses are strongly advised by Compliance Katta to actively avoid peak business hours and attempt filing early in the morning or late at night. Additionally, keeping time-stamped screenshots of any technical errors can serve as a vital defensive record in case further representations need to be legally made to the GST Grievance Redressal mechanism.

Q.Does Notification No. 01/2026 affect the deadline for quarterly GSTR-3B filers under the QRMP scheme?

The specific deadline extension to April 21, 2026, mentioned in this notification primarily addresses the regular monthly filers whose original statutory deadline was April 20. Taxpayers operating under the QRMP scheme typically have their deadlines on the 22nd or 24th of the month following the quarter, which currently remain strictly unchanged unless further notified by the CBIC.