Decoding Reverse Charge Mechanism (RCM) in GST: When the Recipient Becomes the Taxpayer

In the world of Goods and Services Tax (GST), we're generally used to a straightforward rule: the seller (or supplier) charges GST from the buyer (or recipient) and then pays it to the government. Simple, right?

Well, like many tax laws, GST has its exceptions. One significant exception, and often a point of confusion for many businesses, is the Reverse Charge Mechanism (RCM). This unique rule flips the script entirely, making the recipient of goods or services responsible for paying the GST directly to the government, instead of the supplier.

Let's break down RCM in simple terms, explore why it exists, and most importantly, identify the situations where you, as a recipient, might suddenly find yourself liable for GST payment.

What is GST (A Quick Recap)?

Before diving into RCM, let's quickly remember what GST is. It's a consumption-based tax levied on the supply of most goods and services. The idea is to have a seamless tax system from manufacturing to consumption, avoiding the cascading effect of taxes. In most cases, the supplier collects GST from the buyer and deposits it with the tax authorities.

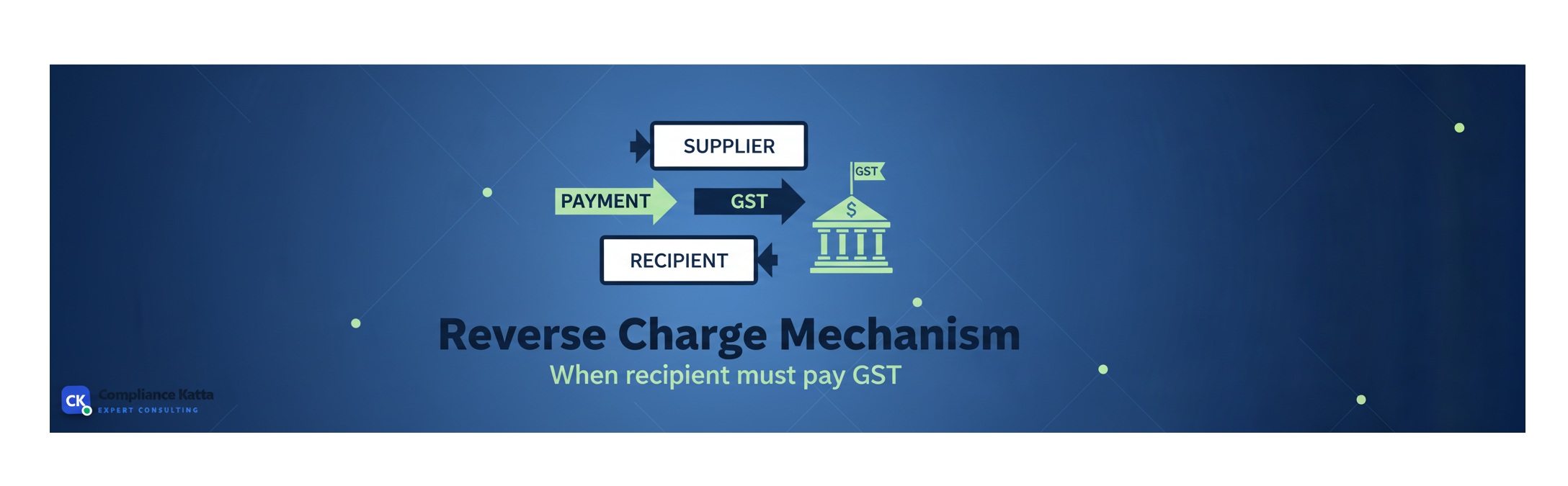

Normal GST vs. Reverse Charge Mechanism: The Big Difference

Imagine you buy a new laptop. The store adds GST to your bill, and you pay the total amount. The store then pays that GST to the government. This is the forward charge mechanism – the standard way GST works.

Now, imagine you hire a specific type of service, say, a lawyer for your business. Under RCM, the lawyer might not charge you GST on their invoice. Instead, you, as the recipient of the legal service, are expected to calculate the GST, pay it directly to the government, and then you might even be able to claim it back as Input Tax Credit (ITC) if you're eligible. This is the Reverse Charge Mechanism.

Why Does RCM Exist? The Logic Behind It

The government introduced RCM for several practical reasons:

- To Broaden the Tax Net: It helps collect tax from unorganized sectors or small suppliers who might otherwise be difficult to track or enforce compliance upon.

- Simplifying Tax Collection: For certain services, especially imports, it's easier to collect tax from the organized recipient rather than a foreign supplier.

- Preventing Tax Evasion: In specific scenarios, RCM helps ensure that tax is definitely paid, even if the supplier is reluctant or avoids compliance.

- Leveling the Playing Field: It ensures that all businesses, whether dealing with registered or unregistered suppliers (in certain cases), are subject to the same tax treatment.

Key Situations Where Reverse Charge Mechanism Applies

RCM isn't a blanket rule; it applies to specific goods and services, as notified by the government under Section 9(3) and Section 9(4) of the CGST Act. Here are some of the most common and important scenarios:

1. Goods Transport Agency (GTA) Services

If you're a business (a registered person) receiving services from a Goods Transport Agency (a person who provides service in relation to transport of goods by road in a goods carriage), you are usually liable to pay GST under RCM. The GTA typically has the option to charge forward or reverse, but for most businesses, it falls under RCM.

2. Legal Services

When a business (or any body corporate) receives legal services from an individual advocate, senior advocate, or an arbitral tribunal, the recipient is required to pay GST under RCM. This means if your company hires a lawyer, your company pays the GST directly.

3. Import of Services

If you're a business in India importing any service from outside India (e.g., software development from a U.S. company, consultancy from a UK firm), you, as the importer (recipient), must pay GST under RCM.

4. Services by Government or Local Authority

Generally, services provided by the government are exempt. However, if a registered person receives services from the government or a local authority (excluding renting of immovable property, services by Department of Posts, and services in relation to an aircraft or a vessel inside or outside the precincts of a port or airport), the recipient is liable to pay GST under RCM.

5. Services by a Director to a Company/Body Corporate

If a director, in their capacity as a director, provides services to the company or body corporate, the company or body corporate is liable to pay GST under RCM on the remuneration paid to the director (excluding salary part which is subject to TDS).

6. Services by an Insurance Agent

When an insurance agent provides services to any person carrying on insurance business, the insurance company is liable to pay GST under RCM.

7. Services by a Recovery Agent

If a recovery agent provides services to a banking company, financial institution, or a non-banking financial company (NBFC), the banking company, financial institution, or NBFC is liable to pay GST under RCM.

8. Certain Supplies by Unregistered Persons to Registered Persons (Specific Cases)

While the general provision for RCM on supplies from unregistered persons was largely suspended, it still applies in very specific, notified circumstances. For example, a promoter receiving specified goods or services for construction from an unregistered supplier might be liable to pay GST under RCM.

9. Services through an E-commerce Operator

For certain services like passenger transport, accommodation, housekeeping, and restaurant services, if they are supplied through an e-commerce operator, the e-commerce operator itself is liable to pay GST. This is a special type of RCM where the e-commerce operator, not the actual service provider, collects and pays the tax.

How Does RCM Work in Practice?

If you're a registered business and RCM applies to a transaction you're involved in, here's the general process:

- Identify RCM: Recognize that the supply you're receiving falls under the RCM provisions.

- Self-Invoice: If the supplier is unregistered, you might need to issue a 'self-invoice' for the goods or services received.

- Calculate & Pay GST: Calculate the applicable GST on the value of the supply. You then pay this GST directly to the government, usually using cash ledger balance.

- Claim Input Tax Credit (ITC): The good news is that if you're eligible, you can generally claim the GST paid under RCM as Input Tax Credit in the same month. This means it often becomes a revenue-neutral transaction for eligible businesses, but the compliance burden remains.

Who is Affected by RCM?

- Registered Businesses: Primarily, RCM impacts GST-registered entities who are recipients of specific goods or services.

- Suppliers of Specified Services/Goods: While they don't pay the tax, they must clearly indicate on their invoices that GST is payable under RCM by the recipient.

Benefits and Challenges of RCM

Benefits:

- Wider tax base and improved compliance.

- Reduced burden on small, unorganized suppliers.

- Ensures tax collection on cross-border transactions (import of services).

Challenges:

- Increased compliance burden for recipients (calculating, paying, and claiming ITC).

- Requires thorough understanding of specific RCM provisions to avoid errors.

- Can impact cash flow temporarily for businesses that cannot immediately utilize ITC.

Conclusion

The Reverse Charge Mechanism (RCM) is an integral part of the GST framework, designed to ensure efficient tax collection in specific scenarios. While it might seem a bit complex at first, understanding when and how it applies is crucial for every GST-registered business. Non-compliance can lead to penalties and interest.

Always stay informed about the latest GST notifications and, when in doubt, consult with a tax professional to ensure your business remains compliant and avoids any unnecessary tax liabilities.

Common Questions

Q.What is the main difference between normal GST (forward charge) and Reverse Charge Mechanism (RCM)?

Under normal GST (forward charge), the supplier charges and collects GST from the recipient, then pays it to the government. Under RCM, the recipient of goods or services is directly responsible for calculating and paying the GST to the government, instead of the supplier.

Q.Can I claim Input Tax Credit (ITC) on GST paid under RCM?

Yes, generally, a registered person who pays GST under RCM is eligible to claim that amount as Input Tax Credit (ITC), provided they meet all other conditions for claiming ITC. This makes the transaction revenue-neutral for eligible businesses.

Q.Do I need to issue an invoice if I pay GST under RCM?

If you are a registered person and receive a supply where RCM applies, you must issue a self-invoice for the supply received, especially if the supplier is unregistered. You also need to issue a payment voucher at the time of making payment to the supplier.

Q.Is RCM applicable to all services provided by an unregistered person?

No, the general provision for RCM on supplies from unregistered persons to registered persons (under Section 9(4)) was largely suspended for most goods and services. Currently, it applies only to very specific, notified categories of supplies, such as certain supplies to promoters for construction projects.

Q.What happens if I don't pay GST under RCM when I'm supposed to?

Failure to pay GST under RCM when it's applicable can lead to penalties, interest charges on the unpaid tax amount, and potential legal consequences as per GST law. It's crucial for registered businesses to identify and comply with RCM obligations to avoid these issues.