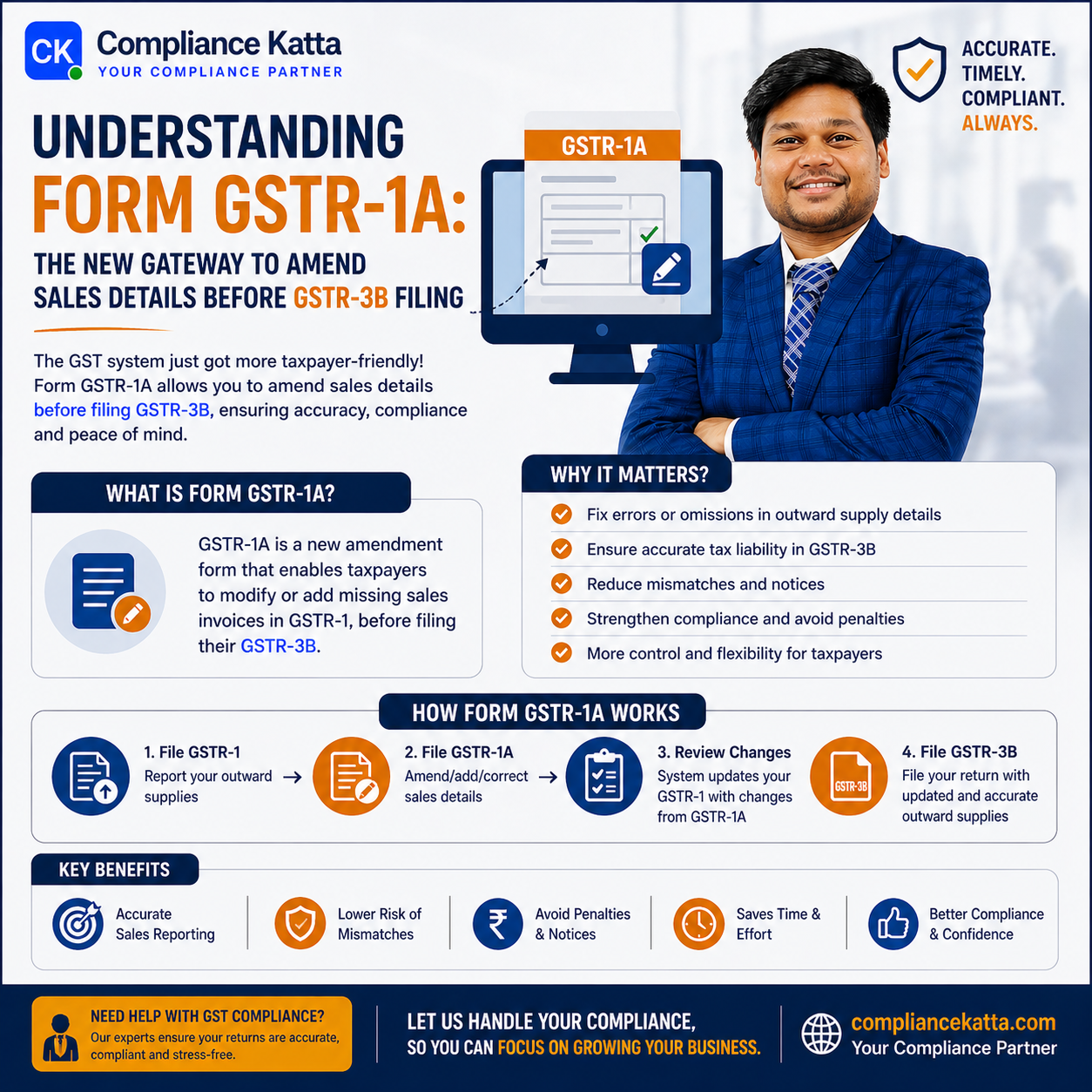

Introduction to Form GSTR-1A

In a significant move to streamline the Goods and Services Tax (GST) return filing process, the Central Board of Indirect Taxes and Customs (CBIC) has introduced Form GSTR-1A. Historically, once a taxpayer filed their GSTR-1 (Statement of Outward Supplies), any errors or omissions could only be rectified in the GSTR-1 of the subsequent tax period. This often led to discrepancies between GSTR-1 and GSTR-3B for the same period, triggering automated notices and potential interest liabilities.

With the introduction of Form GSTR-1A, the GSTN has provided a much-needed window for taxpayers to refine their data. This form allows for the addition, deletion, or modification of details previously submitted in GSTR-1 before the final liability is discharged in GSTR-3B. At Compliance Katta, we believe this is one of the most taxpayer-friendly reforms in recent times, aimed at enhancing the accuracy of self-assessed tax liabilities.

Key Highlights of Form GSTR-1A

- Amendment Window: Taxpayers can amend details filed in GSTR-1 after the due date of GSTR-1 but before filing GSTR-3B for the same period.

- Flexibility: It allows for adding missed invoices, correcting existing invoice details, or deleting wrongly entered data.

- Impact on GSTR-3B: The data modified or added via GSTR-1A will automatically flow into the GSTR-3B of the same tax period, ensuring parity between the two forms.

- Recipient’s GSTR-2B: Changes made in GSTR-1A will reflect in the recipient’s GSTR-2B in the subsequent month, ensuring that the Input Tax Credit (ITC) ecosystem remains updated.

- Optional Nature: While GSTR-1A is an optional facility, it is highly recommended for taxpayers who discover errors shortly after filing GSTR-1.

Professional Tip: Always review your GSTR-1 summary against your books of accounts immediately after filing. If a discrepancy is found, utilize GSTR-1A to avoid receiving DRC-01C notices regarding mismatches between liability declared and paid.

Comparative Analysis: GSTR-1 vs. GSTR-1A

To understand the utility of this new form, let us compare the primary features of GSTR-1 and GSTR-1A:

| Feature | Form GSTR-1 | Form GSTR-1A |

|---|---|---|

| Purpose | Initial declaration of outward supplies. | Amendment of outward supplies for the same period. |

| Timing | Filed by 11th or 13th of the following month. | Between GSTR-1 filing and GSTR-3B filing. |

| Frequency | Monthly or Quarterly (QRMP). | As needed per tax period. |

| Auto-population | Forms GSTR-3B and GSTR-2B. | Updates GSTR-3B of current period; GSTR-2B of next. |

| Mandatory? | Yes. | No (Optional). |

Impact Analysis for Indian Businesses

1. Reduction in System-Generated Notices

The GST portal currently monitors the difference between GSTR-1 and GSTR-3B through Rule 88C. If the liability in GSTR-1 exceeds GSTR-3B by a certain threshold, the taxpayer receives a notice in Form DRC-01B. By using GSTR-1A to align the data before GSTR-3B filing, businesses can proactively prevent these notices.

2. Savings on Interest Liabilities

Before GSTR-1A, if a taxpayer missed reporting an invoice in GSTR-1 but reported it in GSTR-3B, the mismatch could lead to scrutiny. If they missed both and reported in the next month, they were liable to pay 18% interest on the delayed tax payment. GSTR-1A allows for the inclusion of missed invoices in the current month’s liability, potentially reducing the window of interest calculation.

3. Enhanced Credit Flow to Recipients

Since GSTR-1A updates the records, it ensures that recipients receive the correct Input Tax Credit. Although the update in GSTR-2B might happen in the subsequent cycle, the legal record of the supply is corrected much faster than waiting for the next GSTR-1 cycle.

The Workflow of GSTR-1A

- Step 1: File the regular Form GSTR-1 for the tax period.

- Step 2: Discover any errors or missed invoices before filing GSTR-3B.

- Step 3: Open the GSTR-1A dashboard on the GST Portal.

- Step 4: Edit, Add, or Delete records in the relevant tables (B2B, B2C, Exports, etc.).

- Step 5: Review the amended summary and file GSTR-1A.

- Step 6: The corrected values will now reflect in the auto-drafted GSTR-3B.

- Step 7: File GSTR-3B and discharge the final tax liability.

Warning: Once GSTR-3B is filed for a particular tax period, the GSTR-1A window for that period is permanently closed. No further amendments for that period can be made using GSTR-1A.

Compliance Checklist for Taxpayers

- Verify Sales Register: Cross-check the GSTR-1 filed summary with your Sales Register before the 20th of the month.

- Identify Omissions: Check for any credit notes or debit notes that were missed in the initial GSTR-1 filing.

- Calculate Tax Liability: Ensure that the total tax liability after GSTR-1A matches the cash and credit balance available for GSTR-3B.

- Monitor Recipient Communication: Inform your major B2B clients if you have used GSTR-1A to correct their invoice details to avoid reconciliation issues at their end.

- Ensure Timely Filing: Remember that GSTR-1A must be filed before the GSTR-3B deadline (usually the 20th or 22nd/24th for QRMP) to be effective.

Conclusion

The introduction of Form GSTR-1A is a landmark reform by the CBIC that provides taxpayers with the flexibility to correct their records in near real-time. By bridging the gap between the statement of supplies and the summary return, GSTN has simplified the compliance burden and reduced the scope for clerical errors leading to legal disputes. Businesses should integrate GSTR-1A review into their monthly closing process to ensure a robust and error-free GST compliance framework. For expert assistance in managing your GST returns, Compliance Katta remains your trusted partner in navigating the evolving landscape of Indian taxation.

Common Questions

Q.What is the primary benefit of filing GSTR-1A?

The primary benefit of GSTR-1A is that it allows taxpayers to correct errors or add missed invoices from their GSTR-1 before they file GSTR-3B. This ensures that the tax liability declared in GSTR-3B is accurate and matches the sales data, thereby avoiding system-generated mismatch notices like DRC-01B.

Q.Is GSTR-1A a mandatory filing for all GST taxpayers?

No, GSTR-1A is not mandatory. It is an optional facility provided to taxpayers who wish to amend their sales details after filing GSTR-1 but before filing GSTR-3B for the same period. If your GSTR-1 is already correct, you do not need to file GSTR-1A.

Q.Can I file GSTR-1A after I have already filed GSTR-3B for the month?

No, the GSTR-1A facility is only available for the window between the filing of GSTR-1 and the filing of GSTR-3B. Once GSTR-3B is submitted, the GST portal locks the data for that period, and any further amendments can only be made in the GSTR-1 of the subsequent tax period.

Q.How does GSTR-1A affect the Input Tax Credit (ITC) of my customers?

Amendments made through GSTR-1A will be reflected in the recipient's GSTR-2B. However, it is important to note that these changes usually reflect in the GSTR-2B of the month following the one in which GSTR-1A was filed. This ensures the recipient eventually gets the correct credit without the supplier having to wait for the next month's return cycle.

Q.Can QRMP taxpayers use the GSTR-1A facility?

Yes, the GSTR-1A facility is available for both regular monthly filers and those under the Quarterly Return Monthly Payment (QRMP) scheme. QRMP filers can use it to amend details filed through the Invoice Furnishing Facility (IFF) or the quarterly GSTR-1 before they file their quarterly GSTR-3B.