What is Input Tax Credit (ITC)? The Foundation of Savings

Imagine you buy raw materials for your business and pay GST on them. Then, you use these materials to make a final product, which you sell, collecting GST from your customers. Without Input Tax Credit (ITC), you'd essentially be paying tax on tax – a 'cascading effect' that makes things more expensive for everyone.

ITC is a brilliant mechanism under GST that allows businesses to reduce their final tax liability by the amount of tax they have already paid on their inputs (goods or services) used in the course or furtherance of business. Think of it as getting a credit for the GST you've already paid, which you can then use to offset the GST you owe on your sales.

Why Is ITC Crucial for Your Business?

- Cost Reduction: Directly lowers your operational costs.

- Competitive Pricing: Allows you to price your products/services more competitively.

- Cash Flow Improvement: Reduces the cash outflow for tax payments.

- Fair Taxation: Prevents the cascading effect of taxes, ensuring tax is levied only on the value addition at each stage.

Demystifying Section 16: The Core Conditions for Claiming ITC

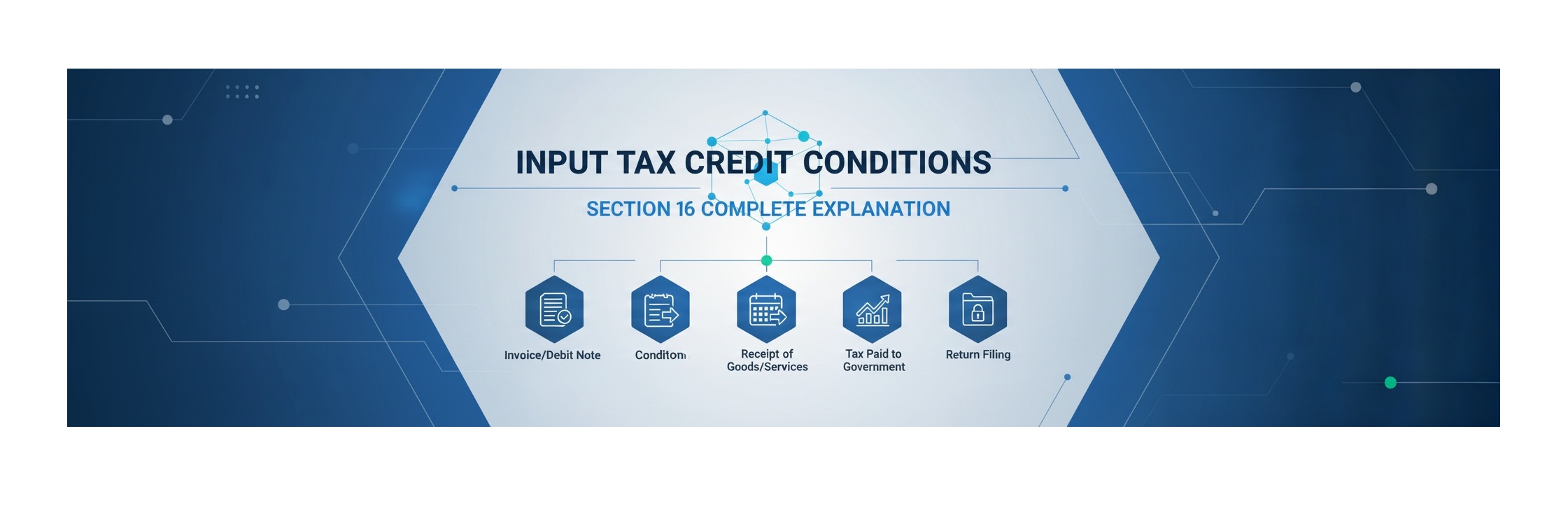

Section 16 of the Central Goods and Services Tax (CGST) Act, 2017, is the bedrock for claiming ITC. It lays down specific conditions that every registered person must satisfy to be eligible for this credit. Let's break them down in simple terms:

1. You Must Have a Valid Tax Document (Invoice or Debit Note)

This is the first and most fundamental condition. To claim ITC, you must possess a valid document issued by your supplier. This typically means:

- A tax invoice issued by a registered supplier.

- A debit note issued by a supplier.

- A bill of entry (for imported goods).

- An invoice issued by you (if you're paying tax under the reverse charge mechanism).

- A document issued by an Input Service Distributor (ISD).

Key takeaway: No proper document, no ITC. Always ensure your supplier provides a GST-compliant invoice.

2. You Must Have Received the Goods or Services

It's not enough to just have an invoice; you must actually receive the goods or services for which you are claiming ITC. This can be directly by you or by another person on your direction (bill-to-ship-to model).

What if goods are received in installments? You can claim the full ITC only after the last lot or installment of goods is received.

Key takeaway: Physical receipt or deemed receipt is mandatory.

3. The Supplier Must Have Paid the Tax to the Government

This is a critical condition to prevent fraudulent claims. The GST charged by your supplier on the invoice must actually be paid by them to the government. This condition is largely verified through the reconciliation of GSTR-2A/2B with your purchase records.

Key takeaway: Your ITC claim is linked to your supplier's compliance. Choose reliable suppliers.

4. You Must File Your GST Returns

To claim ITC, you must furnish a valid GST return, typically GSTR-3B. The details of the ITC claimed should be reflected in your returns.

Key takeaway: Regular and timely filing of GST returns is essential for ITC eligibility.

Important Nuances & Special Cases (Provisos to Section 16(2))

The 180-Day Payment Rule

If you, as the recipient, fail to pay the value of the supply (along with the tax due) to your supplier within 180 days from the date of the invoice, you must reverse the ITC you claimed on that supply. This reversed ITC needs to be added to your output tax liability, along with interest.

However, once you make the payment to the supplier, you can reclaim the ITC. This rule doesn't apply to supplies where tax is payable under the reverse charge mechanism.

Key takeaway: Pay your suppliers on time to avoid ITC reversal and interest.

No Depreciation on GST Component

If you claim depreciation on the tax component of a capital good or plant and machinery under the Income Tax Act, you cannot claim ITC on that same tax component under GST. It's either one or the other, not both.

Key takeaway: Avoid double benefits – choose between depreciation under IT Act or ITC under GST Act for the tax portion.

The Time Limit for Claiming ITC (Section 16(4))

There's a deadline for claiming ITC! You cannot claim ITC for an invoice or debit note after:

- The 30th day of November following the end of the financial year to which such invoice or debit note pertains, OR

- The date of furnishing of the relevant annual return, whichever is earlier.

For example, for invoices related to FY 2023-24, the deadline to claim ITC would be 30th November 2024 or the date of filing your annual return for FY 2023-24 (GSTR-9), whichever comes first.

Key takeaway: Don't procrastinate! Claim your ITC within the stipulated time to avoid losing it.

What Happens If You Don't Meet the Conditions?

Failing to meet any of these conditions can lead to:

- Disallowance of ITC: You won't be able to claim the credit, increasing your tax liability.

- Reversal of ITC: If you claimed it incorrectly, you'll have to reverse it, potentially with interest and penalties.

- Increased Cash Outflow: More tax payable from your pocket.

- Compliance Issues: Can lead to scrutiny from tax authorities.

Staying Compliant and Maximizing Your ITC

To ensure you meet all ITC conditions and maximize your savings:

- Maintain Proper Records: Keep all tax invoices and debit notes meticulously.

- Regular Reconciliation: Match your purchase register with GSTR-2A/2B regularly.

- Timely Payments: Ensure payments to suppliers are made within 180 days.

- File Returns Promptly: Submit your GSTR-3B and annual returns on time.

- Choose Compliant Suppliers: Work with suppliers who regularly file their GST returns.

- Seek Professional Help: If in doubt, consult with GST experts.

Conclusion

Input Tax Credit is a cornerstone of the GST regime, designed to make taxation fair and efficient. Understanding and adhering to the conditions laid out in Section 16 of the CGST Act, 2017, is not just about compliance; it's about smart financial management for your business. By carefully managing your invoices, payments, and returns, you can effectively claim your rightful ITC and significantly reduce your tax burden. Don't let valuable credits slip away – stay informed and stay compliant!

Common Questions

Q.What is Input Tax Credit (ITC) in simple terms?

Input Tax Credit (ITC) allows businesses to reduce their final GST liability by the amount of GST they have already paid on their purchases (inputs, input services, or capital goods) used for business purposes. It prevents the 'tax on tax' effect.

Q.What are the four main conditions under Section 16 for claiming ITC?

The four main conditions are: 1) Possessing a valid tax invoice or debit note, 2) Receiving the goods or services, 3) The supplier having actually paid the tax to the government, and 4) Filing your valid GST returns.

Q.What is the '180-day rule' for ITC, and what happens if I don't follow it?

The 180-day rule states that if you don't pay your supplier for a supply (including tax) within 180 days of the invoice date, you must reverse the ITC you claimed, along with interest. You can reclaim the ITC once you make the payment.

Q.Is there a time limit to claim Input Tax Credit under GST?

Yes, you cannot claim ITC for an invoice or debit note after the 30th day of November following the end of the financial year to which the invoice pertains, or the date of furnishing of the relevant annual return, whichever is earlier.

Q.Can I claim ITC if my supplier hasn't paid the GST to the government?

No, one of the crucial conditions under Section 16 is that your supplier must have actually paid the GST collected from you to the government. If they haven't, your ITC claim for that supply may be disallowed or reversed.