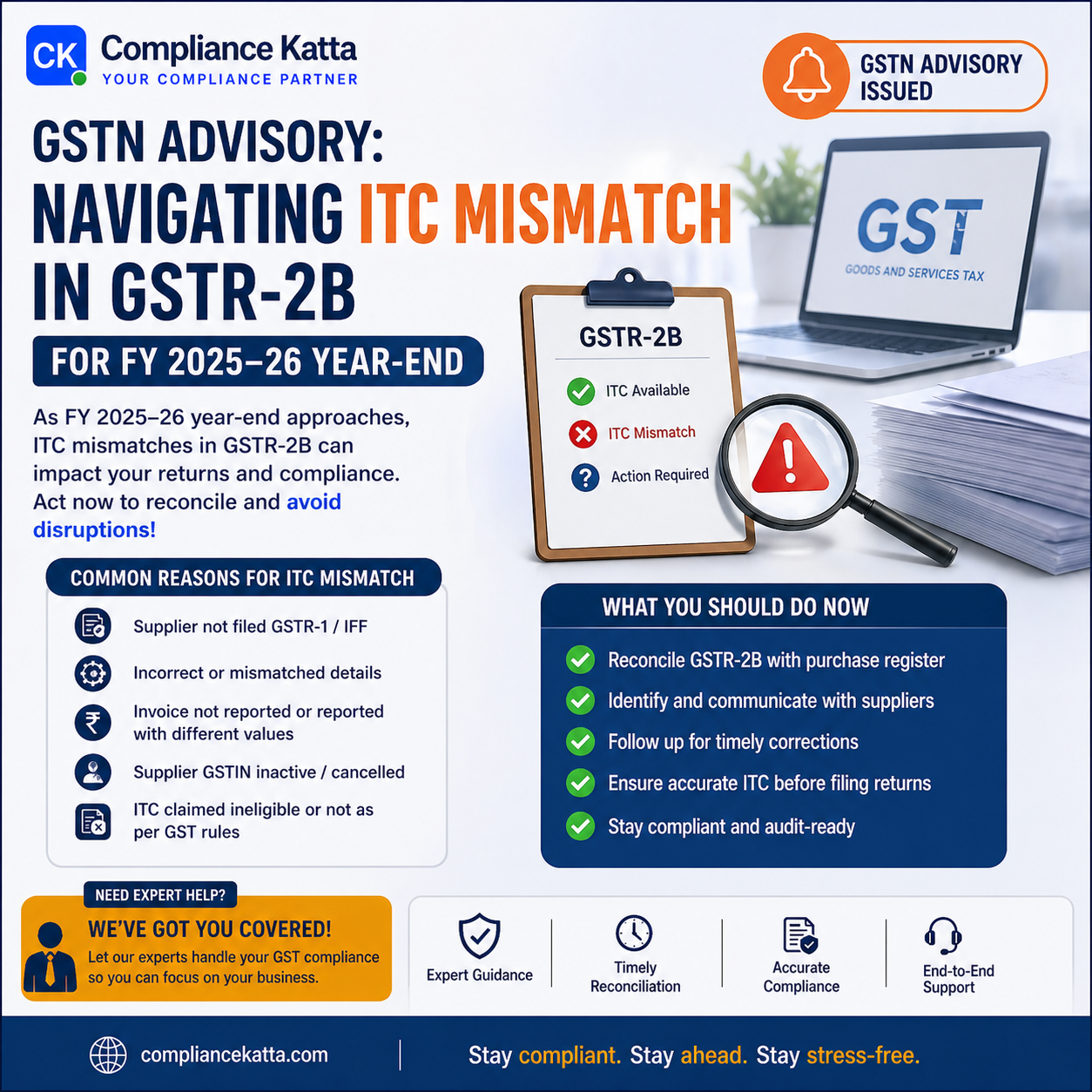

Introduction to the GSTN Advisory for FY 2025-26

As the financial year 2025-26 draws to a close, the Goods and Services Tax Network (GSTN) has issued a vital advisory addressing the growing concerns among taxpayers regarding Input Tax Credit (ITC) auto-population in GSTR-3B. With the integration of tighter system-driven checks, many businesses are noticing discrepancies in their GSTR-2B, specifically regarding invoices dated prior to April 2025 but reported by suppliers in the current window. This advisory clarifies the application of the revised Section 16(4) logic within the GST portal, which acts as a gatekeeper for ITC eligibility.

The Core Confusion: Why ITC is being Restricted

The primary source of friction arises from the auto-population logic that now strictly enforces the deadlines prescribed under Section 16(4) of the CGST Act. For the financial year 2024-25, the deadline to claim ITC was the 30th of November 2025. When suppliers file their GSTR-1 late for those older invoices during the March 2026 period, the GST portal automatically flags this credit as 'Ineligible' in the recipient's GSTR-2B. At Compliance Katta, we emphasize that understanding this automated restriction is crucial for accurate year-end book-closing.

Key Highlights of the GSTN Advisory

- System-Driven Restriction: The GSTR-2B now features a robust mechanism that categorizes ITC into 'Available' and 'Not Available' based on the date of the invoice and the date of filing by the supplier.

- Section 16(4) Enforcement: ITC pertaining to invoices of FY 2024-25 reported after November 30, 2025, will be permanently blocked from auto-populating as eligible credit.

- GSTR-3B Auto-population: Only the 'Available' portion of ITC from GSTR-2B will flow into the GSTR-3B table 4(A), potentially leading to a higher cash tax liability for businesses unaware of these late filings.

- Impact on FY 2025-26: Invoices issued during FY 2025-26 must be reported by suppliers before the upcoming November 2026 deadline to avoid similar issues in the next cycle.

- Clarification on Amendments: The advisory also touches upon how amendments to old invoices are treated under the current validation logic.

Professional Tip: Always cross-verify the 'ITC Not Available' section of your GSTR-2B. Often, taxpayers only look at the summary, missing out on the reasons why certain credits were denied by the system.

Detailed Impact Analysis

The implications of this advisory are far-reaching for Indian businesses. The sudden realization that expected ITC is ineligible can cause significant cash flow disruptions. Furthermore, if a taxpayer manually overrides the GSTR-3B figures to claim restricted ITC, they risk receiving automated notices (GST DRC-01C) for ITC mismatches. This creates a high-friction environment during annual audits.

Comparison of ITC Eligibility Logic

| Invoice Period | Supplier Filing Date | GSTR-2B Status | ITC Eligibility |

|---|---|---|---|

| FY 2024-25 | Before 30-Nov-2025 | Available | Eligible |

| FY 2024-25 | After 30-Nov-2025 | Not Available | Ineligible (Sec 16(4)) |

| FY 2025-26 | Within Due Date | Available | Eligible |

| FY 2025-26 | Delayed Filing | Available* | Subject to 16(4) in 2026 |

*Note: Eligibility for FY 2025-26 invoices remains intact until the November 2026 deadline.

Reconciliation Flowchart

1. Download GSTR-2B for March 2026.2. Identify invoices marked as 'Ineligible' due to Section 16(4).3. Compare GSTR-2B with the Internal Purchase Register (PR).4. Communicate with suppliers who filed FY 2024-25 invoices late.5. Adjust the books of accounts to reverse ineligible ITC or treat it as an expense.Compliance Checklist for Year-End Closing

To ensure a smooth transition and minimize litigation risks, Compliance Katta recommends the following actionable steps:

- Verify Supplier Filing Status: Regularly use the 'Search Taxpayer' tool to check the filing frequency and consistency of your key vendors.

- Reconcile Monthly: Do not wait for the year-end. Monthly reconciliation between GSTR-2B and your Purchase Register is now mandatory for survival.

- Calculate Cash Flow Impact: If significant ITC is restricted in GSTR-2B, calculate the additional cash outflow required for the March 2026 GSTR-3B filing in advance.

- Ensure Proper Documentation: Maintain a log of all communications with suppliers regarding delayed filings for future representation before tax authorities.

- Audit Ineligible ITC: Specifically check Table 4(D)(2) of GSTR-3B to ensure that ineligible ITC is correctly reported as per the law, avoiding future scrutiny.

- Update Purchase Agreements: Include clauses that allow for the recovery of GST amounts from suppliers if ITC is lost due to their delayed filing beyond Section 16(4) deadlines.

Conclusion

The GSTN advisory is a reminder that the GST ecosystem is becoming increasingly automated and intolerant of compliance delays. For FY 2025-26, businesses must be proactive in their reconciliation processes. Relying solely on auto-populated data without understanding the underlying logic of Section 16(4) can lead to financial losses and legal complications. By following the roadmap provided by Compliance Katta, taxpayers can navigate these year-end challenges with confidence and precision.

Common Questions

Q.What does Section 16(4) of the CGST Act specify regarding ITC deadlines?

Section 16(4) stipulates that a registered person cannot claim Input Tax Credit for an invoice or debit note after the 30th of November following the end of the financial year to which such invoice pertains, or the date of filing the relevant annual return, whichever is earlier. For FY 2024-25, this means any credit not reflected or reported by November 30, 2025, becomes technically ineligible.

Q.Why is my GSTR-2B showing 'ITC Not Available' for recent supplier filings?

If the supplier has filed an invoice dated in a previous financial year (e.g., FY 2024-25) after the legal deadline of November 30, 2025, the GST portal's logic automatically marks that credit as 'Not Available'. This is because the system is programmed to enforce Section 16(4) restrictions automatically, preventing taxpayers from claiming expired credits.

Q.Can I manually add the missing ITC in GSTR-3B if it is restricted in GSTR-2B?

While the GSTR-3B allows for manual editing of ITC cells, doing so when the system has restricted the credit in GSTR-2B will trigger a red flag. You will likely receive a DRC-01C notice requiring you to explain the difference, and since the restriction is based on law (Section 16(4)), manual claims are generally not sustainable and may lead to interest and penalties.

Q.How should I handle suppliers who file invoices late?

You should maintain a robust vendor management system. If a supplier files an invoice after the Section 16(4) deadline, the GST paid to them becomes a cost to your business. It is advisable to have indemnity clauses in your contracts with suppliers to recover such lost ITC amounts from their pending payments.

Q.Does this advisory affect the ITC for the current financial year 2025-26?

The advisory primarily clarifies why older invoices (FY 2024-25) are currently showing as ineligible. For invoices issued within FY 2025-26, you have until November 30, 2026, to ensure they are reported by your suppliers. However, the logic explained in the advisory will apply to FY 2025-26 invoices if they are reported after that future deadline.